Q&A with the World Economic Forum on New Retail Investor Trends

Norkon Team

Norkon Team If you work in financial media, fintech, investor relations, asset management or policy, you’re already serving a new audience – one that’s younger, more diverse, more digital and more self-directed than the retail investors who came before.

Today’s individual investor looks very different from a decade ago: Gen Z retail investors track markets on their phones on the go, first-time private investors are building portfolios through digital trading apps, and across the globe, people are turning to stock markets to build personal financial resilience.

The environment raises fundamental questions for the entire financial ecosystem:

- What happens when people learn about investing on social platforms before they ever encounter a trusted news outlet?

- If younger retail investors feel more confident with crypto than with bonds or ETFs, what does that say about how we explain traditional finance?

- As more private investors turn to AI chatbots for guidance, what becomes of human advisors, journalists and educators?

The motivation behind this trend is not speculation. When surveyed, most retail investors say they’re investing to secure long-term goals and build a basic safety net in an uncertain world of strained public finances and evolving pension systems (source: 2024 Global Retail Investor Outlook, World Economic Forum). For anyone who informs, educates or influences private investors, it’s both a powerful opportunity and a responsibility.

This blog post explores how retail investors are learning, why confidence and understanding don’t always align, and what role trusted financial media should play in a landscape where social platforms and AI chatbots have become the first point of contact.

How retail investors are rewriting the rules of financial communication

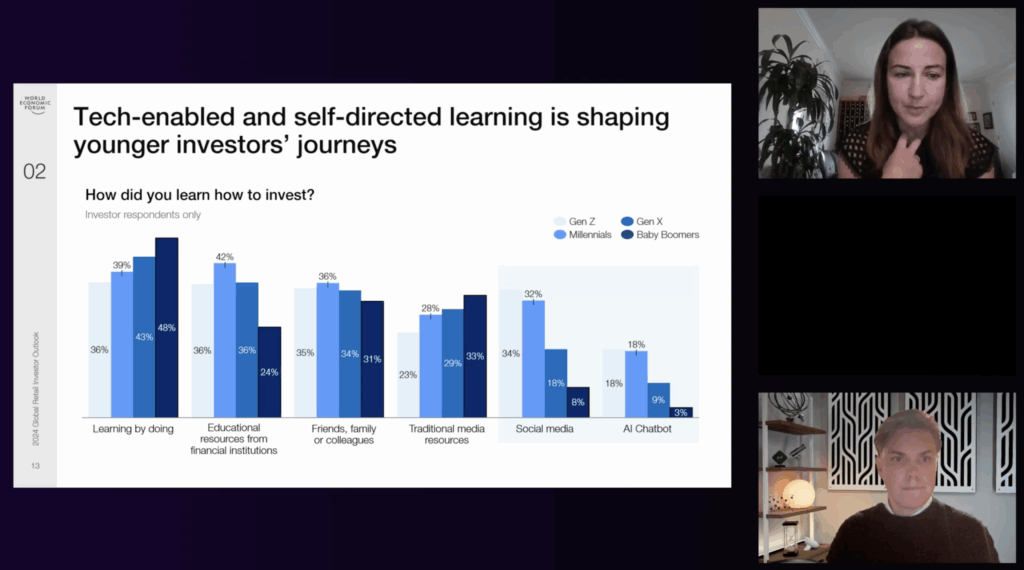

One of the most striking findings from the research is how people today are learning to invest.

Younger investors consistently report learning from:

- Social media and influencers

- Friends and family

- Apps and user-friendly digital platforms

- Increasingly, AI chatbots

Traditional financial advisors, by contrast, are far more common among older individual investors.

Part of this is simple accessibility. In many markets, professional advice either doesn’t exist for smaller private investor portfolios or feels too intimidating and formal: the classic “man in a tie in an office you need an appointment to see.”

Social platforms, by contrast, are immediate, conversational and familiar. People see someone who looks like them, sounds like them, and invests with the same constraints. However, the problem is that many “finfluencers” are rewarded for engagement, not actual financial outcomes. So while the advice gap is being filled, it’s not always with high-quality information as the incentives are misaligned.

Insights from the World Economic Forum research on young investor behaviour, 2024

For financial media, there are clear takeaways and lessons to borrow from what social platforms do well:

- Plain language over technical jargon

- Dialogue over lectures

- Personal, human stories over abstract concepts

- Short, digestible content formats that lead to deeper learning

When confidence and reality don’t match

Another signal from the World Economic Forum’s research: many private investors feel more confident navigating cryptocurrencies than ETFs, bonds or even stocks.

Crypto has enjoyed years of simple, repetitive messaging. Traditional financial instruments, meanwhile, are often presented with dense terminology and complex explanations.

Confidence tends to follow clarity, not importance.

That gap matters. Without accessible explanations of how inflation, interest rates or asset classes work, private investors make decisions based on perception instead of fundamentals.

This is where financial media has a crucial role to play:

- Demystify core portfolio building blocks

- Make macro shifts understandable at the household level

- Create spaces where it’s safe to admit “I don’t understand this – yet”

When perceived understanding is higher for crypto than for bonds, it signals that the problem isn’t the retail investor but the way we communicate.

Q&A with Natalya Guseva from the World Economic Forum

During a recent webinar, we had the opportunity to pick the brain from Natalya Guseva, Head of Financial Markets and Resilience Initiatives at the World Economic Forum and explore what the most recent retail investor behaviors means for financial news publishers.

Norkon: How does early exposure to investing shape financial behavior?

N.G.:

I think early exposure creates early engagement with one’s financial goals, and that’s such a positive thing. Talking about money is important: we all need money for everything we do in life. Starting early in thinking about financial decisions also extends retail investors’ time in markets and their ability to weather different cycles.

There are, of course, some potential incentive misalignments with some “finfluencers” whose rewards are based on clicks and engagement rather than private investor outcomes.

So a lesson for more traditional financial institutions is how to communicate and reach their readers – or their future subscribers. It’s not about eliminating social media, but learning from the elements that resonate: accessibility, tone and format.

What role should media organizations play in bridging the advice gap and countering misinformation around investing, while still engaging younger audiences?

N.G.:

Great question. Cost, ease of access and ease of understanding matter deeply to individual investors. I’m not saying everything should be free – “free” comes with its own trade-offs – but there should be real value in access and understanding.

That means using less jargon and fewer technical terms, meeting retail investors where they are, and presenting information in short, personalized and relatable formats – these are really key. Many people don’t understand what an ETF is simply because of the terminology. Even bonds, for example, were perceived differently between 2022 and 2024, mostly due to inflation and interest rate changes, which led private investors to see bonds as volatile and untrustworthy.

So to actually answer your question, I think there’s something around being accessible, not using jargon, focusing on outcomes, and explaining in a way that’s clear and not talking down.

But I also think that for traditional media sources, the next layer of competition might not be social media: it might be the AI chatbot and AI agent. Just like Netflix said its competition wasn’t TV but sleep, right? That’s the new horizon.

You’ve been closely involved in how banking, markets and investor behavior have evolved over time. In your view, how can trusted financial media help people become more financially educated and independent?

N.G.:

“Financial education” or “literacy” can sound patronizing, as if one party is the expert and the other must be corrected. So I would reframe it a little: how do we destigmatize the conversation around money? Many people don’t feel comfortable talking about money – uncertanties vary across genders, cultures and geographies.

So, how do you make it more commonplace and normalize the topic? Once you start talking about it, everything else follows and becomes educational almost by default.

At the same time, we shouldn’t place all responsibility on individuals. Financial independence is great, and being your own Chief Investment Officer may work for some, but most people have jobs and families, and it can become burdensome to feel they need to learn about every stock and bond out there, about portfolio construction, and so on. That’s not necessary. So, there’s plenty that can be done to think through it and see what traditional financial institutions can do, what capital aggregators can do, and so on. There’s a big role for asset managers, pensions and others here as well.

As more people around the world start investing, how do you see regulators, financial institutions and the media work together to improve financial literacy and build trust and even protect investors?

N.G.:

This is the trillion dollar question because collaboration here is vital. No single actor can really address this holistically. Governments are stretched, workplace pensions are less prevalent in parts of the world.

There’s a need for people to actually secure their financial futures, and work to be done in collaborating around engendering trust. And as we saw, trust in general is declining, which is worrisome.

But we see that employers, especially large employers, usually have the trust of their employees. Of course, they’re there for the paycheck, but employers frequently are also an intermediary to other benefits whether it’s pension, insurances or other financial products. So there lies an opportunity.

What’s needed is collective focus on trust, confidence and empowerment – delivered without patronizing tone. Individuals and families are trying to plan and secure their futures. With so many competing priorities in government agendas, the challenge is to retain a human-centric focus: people’s financial security should remain at the center.

Watch the full webinar for insights into retail investors behaviours and takeaways.